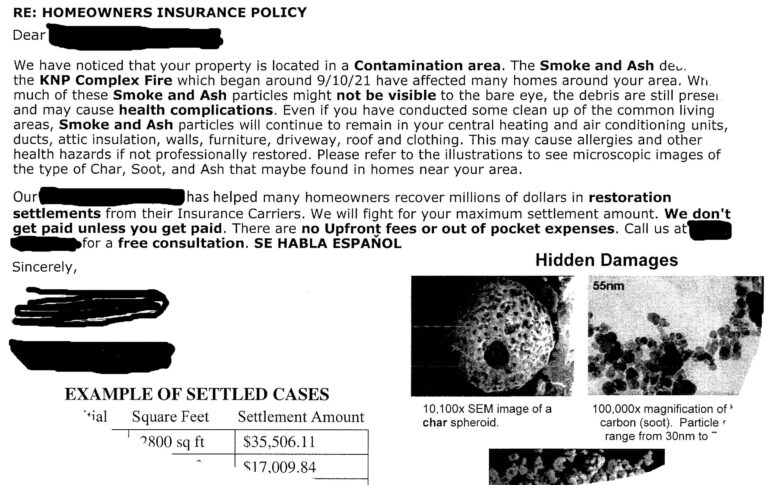

Recently Mennonite Aid Plan has received a number of claims from people in the Fresno/Sanger/Reedley area for smoke damage from the Creek Fire last year. Smoke is a covered cause of loss, but there has to be actual damage for us to pay a claim. What will happen if you file a claim is that we will schedule a smoke detection company to assess whether there is smoke damage. They will take samples from inside and outside your home and send them to a laboratory for testing. If the tests and photos show nominal amounts of smoke and dust, there is no damage and therefore nothing to pay. This will be a claim on your policy. Our advice is that if you believe you have smoke damage, turn in a claim. If you are being encouraged to turn in a claim from an outside source and hadn’t noticed anything before, you might reconsider.